Accountancy : Company Accounts and Analysis of Financial Statements 2012 CBSE [ All India ] Set 2

To Access the full content, Please Purchase

-

Q1

Name an item which is never shown on the ‘Payments’ side of ‘Receipts and Payments Account’, but is shown as an Expense while preparing ‘Income and Expenditure Account’.

Marks:1View AnswerAnswer:

Depreciation on Fixed Assets.

-

Q2

A partnership deed provides for the payments of interest on capital but there was a loss instead of profit during the year 2010-2011. At what rate, will the interest on capital be allowed?

Marks:1View AnswerAnswer:

In case of loss, no interest on capital is allowed as it is an appropriation of profits.

-

Q3

Give any one distinction between sacrificing ratio and gaining ratio.

Marks:1View AnswerAnswer:

Sacrificing ratio is calculated at the time of admission of a partner whereas gaining ratio is calculated at the time of retirement of a partner.

-

Q4

State any one purpose for admitting a new partner in a firm.

Marks:1View AnswerAnswer:

To get more capital.

-

Q5

What is meant by calls in advance?

Marks:1View AnswerAnswer:

Amount paid by shareholders to the company along with application or allotment money, against those calls which are not yet due, is called calls in advance.

-

Q6

From the following information, calculate the amount of subscriptions due to be shown in the ‘Income and Expenditure Account’ for the year ended 31-3-2011 if there are 1000 members and each paying

300 p.a. as subscription:

300 p.a. as subscription:Subscriptions received during the year 2010-2011

3,00,000Subscriptions received in advance as on 31-3-2011

36,800Subscriptions outstanding as on 1-4-2010

32,000Subscriptions received in advance as on 1-4-2010

25,000Marks:3View AnswerAnswer:

Calculation of amount to be shown in Income and Expenditure Account:

Particulars

Subscription received during the year

3,00,000

Add: Outstanding subscription as on 31-3-2011(w.n.)

43,800

Advance subscription as on 1-4-2010

25,000

68,800

3,68,800

Less: Outstanding subscription as on 1-4-2010

32,000

Advance subscription as on 31-3-2011

36,800

68,800

Subscription for the year ending 31-3-2011

3,00,000

W.N.:

Total annual subscriptions (1,000x300) = 3,00,000

Less: Received for current year:-

(3,00,000–36,800–32,000+25,000) = 2,56,200

Outstanding as on 31-3-2011 = 43,800 -

Q7

Sundram Ltd. purchased Furniture for Rs. 3,00,000 from Ravindram Ltd.

1,00,000 were paid by drawing a Promissory Note in favour of Ravindram Ltd. The balance was paid by issue of Equity Shares of 10 each at a premium of 25%.

Pass necessary Journal Entries in the books of Sundram Ltd.Marks:3View AnswerAnswer:

Journal of Sundram Ltd.

Date

Particulars

L.F.

Dr.

Cr.

Furniture A/c Dr.

3,00,000

To Ravindram Ltd.

3,00,000

(For furniture purchased from Ravindram Ltd.)

Ravindram Ltd. Dr.

1,00,000

To Bills Payable A/c

1,00,000

(For bill accepted to pay the amount)

Ravindran Ltd. Dr.

2,00,000

To Equity Share Capital A/c

1,60,000

To Securities Premium A/c

40,000

(For issue of equity shares at a premium of 25%)

W.N.:

Number of equity shares to be issued = 2,00,000 / 12.5 = 16,000 shares

-

Q8

Nav Lakshmi Ltd. invited applications for issuing 3,000, 12% Debentures of

100 each at a premium of 50 per debenture. The full amount was payable on application.

Applications were received for 4,000 debentures. Applications for 1,000 debentures were rejected and the application money was refunded. Debentures were allotted to the remaining applicants.Marks:3View AnswerAnswer:

Journal of Nav Lakshmi Ltd.

Date

Particulars

L.F.

Dr.

Cr.

Bank A/c (4,000x150) Dr.

6,00,000

To Debenture Application A/c

6,00,000

(For application money received with premium)

Debenture Application A/c Dr.

6,00,000

To 12% Debentures A/c (3,000x100)

3,00,000

To Sec. Premium A/c (3,000x50)

1,50,000

To Bank A/c (1,000x150)

1,50,000

(For application money transferred to Debentures Account and Security Premium, and balance refunded)

-

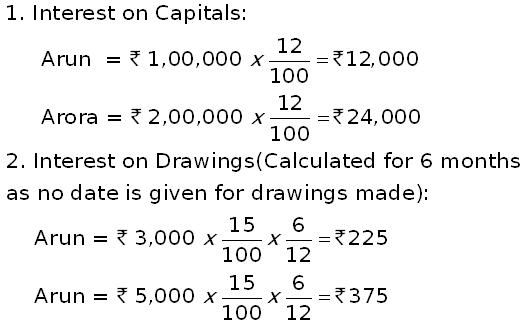

Q9

Lalan and Balan were partners in a firm sharing profits in the ratio of 3:2. Their fixed capitals on 1-4-2010 were: Lalan

1,00,000 and Balan 2,00,000. They agreed to allow interest on capital @ 12% p.a. and to charge on drawings @ 15% p.a. The firm earned a profit before all above adjustments of Rs. 30,000 for the year ended 31.3.2011. The drawings of Lalan and Balan during the year were 3,000 and 5,000 respectively. Showing your calculations clearly, prepare Profit and Loss Appropriation Account of Lalan and Balan. The interest on capital will be allowed even if the firm incurs a loss.Marks:4View AnswerAnswer:

Dr.

Profit and Loss Adjustment Account

for the year ending 31-3-2011

Cr.

Particulars

Particulars

To Interest on Capitals:

By Profit and Loss A/c

30,000

Arun

12,000

By Interest on Drawings:

Arora

24,000

36,000

Lalan

225

Balan

375

600

By Partners Current A/cs(Loss):

Arun

3,240

Arora

2,160

5,400

36,000

36,000

W.N.:

-

Q10

A, B, C and D are partners sharing profits in the ratio of 3:3:2:2 respectively. D retires and A, B and C decide to share the future profits in the ratio of 3:2:1. Goodwill of the firm is valued at

6,00,000. Goodwill already appears in the books at 4,50,000. The profits for the first year after D’s retirement amount to 12,00,000. Give the necessary Journal entries to record Goodwill and to distribute profits. Show your calculations clearly.Marks:4View AnswerAnswer:

Journal Entries

Date

Particulars

L.F.

Dr.

Cr.

A’s Capital A/c Dr.

1,35,000

B’s Capital A/c Dr.

1,35,000

C’s Capital A/c Dr.

90,000

D’s Capital A/c Dr.

90,000

To Goodwill A/c

4,50,000

(Existing goodwill written off in old ratio)

A’s Capital A/c Dr.

1,20,000

B’s Capital A/c Dr.

20,000

To D’s Capital A/c

1,20,000

To C’s Capital A/c

20,000

(Adjustment of new goodwill at the time of retirement of D)

Profit and Loss Appropriation A/c Dr.

12,00,000

To A’s Capital A/c

6,00,000

To B’s Capital A/c

4,00,000

To C’s Capital A/c

2,00,000

(Profit after D’s retirement distributed in new ratio)

W.N.:

1.

2.

3.