Accountancy : Company Accounts and Analysis of Financial Statements 2012 CBSE [ Delhi ] Set 3

To Access the full content, Please Purchase

-

Q1

Name the financial statement prepared by a Not-For-Profit Organisation on accrual basis.

Marks:1View AnswerAnswer:

Income and Expenditure Account.

-

Q2

State the provisions of Indian Partnership Act regarding the payment of remuneration to a partner for the services rendered.

Marks:1View AnswerAnswer:

As per Indian Partnership Act, 1932, in the absence of partnership deed, no remuneration shall be allowed to any partner for his services.

-

Q3

For which share of Goodwill a partner is entitled at the time of his retirement?

Marks:1View AnswerAnswer:

A retiring partner is entitled to get his share, in the goodwill valued at the time of retirement, on the basis of existing profit sharing ratio.

-

Q4

State any two occasions on which a firm can be reconstituted.

Marks:1View AnswerAnswer:

Two occasions may be:

i. Admission of a new partner.

ii. Retirement or death of a partner. -

Q5

Give any one advantage for the redemption of debentures by purchase in the open market?

Marks:1View AnswerAnswer:

It enables the company to redeem the debentures as per its own convenience.

-

Q6

From the following information, calculate the amount of income from subscriptions to be shown in the Income and Expenditure Account for the year ended 31-3-2011:

Subscriptions received during the year 2010-2011

3,40,000

3,40,000Subscriptions outstanding as on 31-3-2011

47,000Subscriptions received in advance as on 31-3-2011

35,000Subscriptions outstanding as on 1-4-2010

28,000Subscriptions received in advance as on 1-4-2010

25,000Marks:3View AnswerAnswer:

Calculation of amount to be shown in Income and Expenditure Account:

Particulars

Subscription received during the year

3,40,000

Add: Outstanding subscription as on 31-3-2011

47,000

Advance subscription as on 1-4-2010

25,000

72,000

4,12,000

Less: Outstanding subscription as on 1-4-2010

28,000

Advance subscription as on 31-3-2011

35,000

63,000

Subscription for the year ending 31-3-2011

3,49,000

-

Q7

Jain Ltd. purchased Building for

10,00,000 from Gupta Ltd. 10% of the payable amount was paid by a cheque drawn in favour of Gupta Ltd. The balance was paid by issue of Equity Shares of 10 each at a discount of 10%.

Pass necessary Journal Entries in the books of Jain Ltd.Marks:3View AnswerAnswer:

Journal of Jain Ltd.

Date

Particulars

L.F.

Dr.

Cr.

Building A/c Dr.

10,00,000

To Gupta Ltd.

10,00,000

(For building purchased from Gupta Ltd.)

Gupta Ltd. Dr.

1,00,000

To Bank A/c

1,00,000

(For 10% of the amount paid through cheque)

Gupta Ltd. Dr.

9,00,000

Discount on Issue of Shares A/c Dr.

1,00,000

To Equity Share Capital A/c

10,00,000

(For issue of equity shares of Rs. 10 each at a discount of Rs. 1)

W.N.:

-

Q8

Narain Laxmi Ltd. invited applications for issuing 7,500, 12% Debentures of

100 each at a premium of 35 per debenture. The full amount was payable on application.

Applications were received for 10,000 debentures. Applications for 2,500 debentures were rejected and the application money was refunded. Debentures were allotted to the remaining applicants.Marks:3View AnswerAnswer:

Journal of Narain Laxmi Ltd.

Particulars

L.F.

Dr.

Cr.

Bank A/c (10,000 x 135) Dr.

13,50,000

To Debenture Application A/c

13,50,000

(For application money received with premium)

Debenture Application A/c Dr.

13,50,000

To 12% Debentures A/c(7,500 x 100)

7,50,000

To Securities Premium A/c(7,500x35)

2,62,500

To Bank A/c

3,37,500

(For application money transferred to Debentures Account and Security Premium, and balance refunded)

-

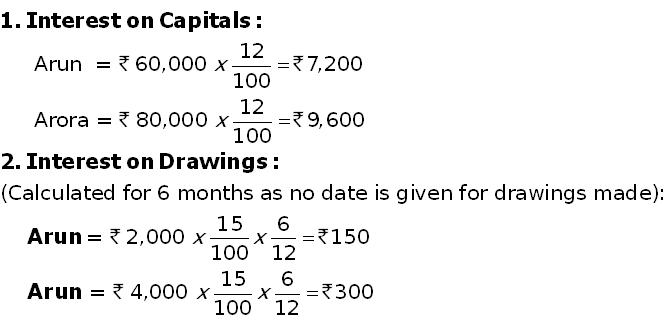

Q9

Arun and Arora were partners in a firm sharing profits in the ratio of 5:3. Their fixed capitals on 1-4-2010 were: Arun

60,000 and Arora 80,000. They agreed to allow interest on capital @ 12% p.a. and to charge interest on drawings @ 15% p.a. The profit of the firm for the year ended 31-3-2011 before all above adjustments were 12,600. The drawings made by Arun were 2,000 and by Arora 4,000 during the year. Prepare Profit and Loss Appropriation Account of Arun and Arora. Show your calculations clearly. The interest on capital will be allowed even if the firm incurs loss.Marks:4View AnswerAnswer:

Dr.

Profit and Loss Adjustment Account

for the year ending 31-3-2011

Cr.

Particulars

Particulars

To Interest on Capitals:

By Profit and Loss A/c

12,600

Arun

7,200

By Interest on Drawings:

Arora

9,600

16,800

Arun

150

Arora

300

450

By Partners Current A/cs(Loss):

Arun

2,344

Arora

1,406

3,750

16,800

16,800

W.N.:

-

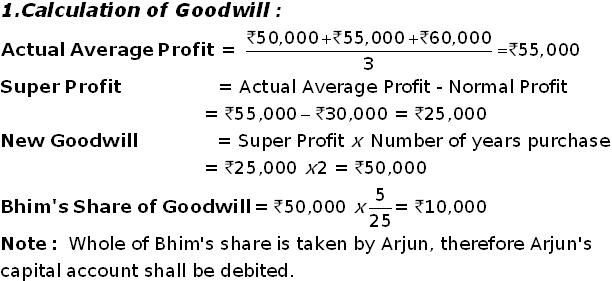

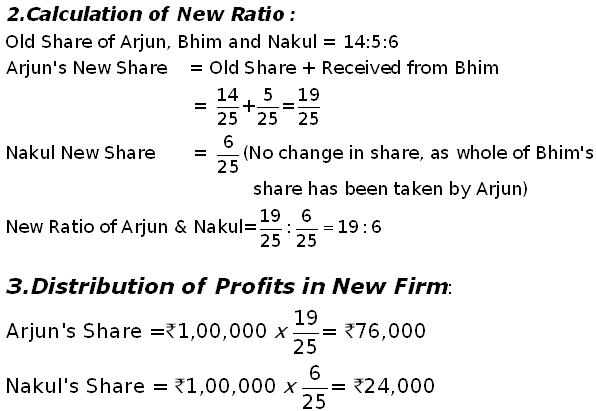

Q10

Arjun, Bhim and Nakul are partners sharing profits & losses in the ratio of 14:5:6 respectively. Bhim retires and surrenders his 5/25th shares in favour of Arjun. The goodwill of the firm is valued at 2 years purchase of super profits based on average profits of last 3 years. The profits for the last 3 years are

50,000, 55,000 & 60,000 respectively. The normal profits for the similar firm are 30,000. Goodwill already appears in the books of the firm at 75,000. The profit for the first year after Bhim’s retirement was 1,00,000. Give the necessary Journal Entries to adjust Goodwill and distribute profits showing your workings.Marks:4View AnswerAnswer:

Journal Entries

Date

Particulars

L.F.

Dr.

Cr.

Arjun’s Capital A/c Dr.

42,000

Bhim’s Capital A/c Dr.

15,000

Nakul’s Capital A/c Dr.

18,000

To Goodwill A/c

75,000

(Existing goodwill written off in old ratio)

Arjun’s Capital A/c Dr.

10,000

To Bhim’s Capital A/c

10,000

(Adjustment of new goodwill at the time of retirement of Bhim)

Profit and Loss Appropriation A/c Dr.

1,00,000

To Arjun’s Capital A/c

76,000

To Nakul’s Capital A/c

24,000

(Profit after Bhim’s retirement distributed in new ratio)

W.N.: